Cissoid, Infineon, ON Semiconductor, Toshiba, and TI discuss the development trends of SiC and GaN in the next five years!

Cissoid, Infineon, ON Semiconductor, Toshiba, and TI discuss the development trends of SiC and GaN in the next five years!

What are the market application trends of SiC and GaN in the next five years?

According to IHS Markit's forecast, the global power semiconductor market will reach US$44.1 billion in 2021, with an annual growth rate of 4.1%. Among them, the Chinese market is expected to be approximately US$15.9 billion, accounting for 36.1% of the global market. Power semiconductors are used in industries such as ultra-high voltage power transmission, big data centers, industrial Internet, intercity high-speed rail, and new energy vehicles and charging piles.

With terminal demand increasing significantly, what are the market opportunities for IGBT, MOSFET, SiC, and GaN devices? In this issue of "International Electronic Business News", analysts and power semiconductor industry practitioners discuss the supply situation and market trends of global power devices.

IGBT and MOSFET are still the mainstream power semiconductors

IC Insights once pointed out in a report that among various types of power semiconductor devices, MOSFET and IGBT modules are the most promising in the short term. In fact, the industry has always held different opinions on "whether there will be a competition pattern of 'you without me' or 'complementary symbiosis' between different power semiconductor devices in the future."

Marketing Director of Infineon Technologies Industrial Power Control Division said:

In this regard, Chen Ziying, marketing director of the Industrial Power Control Division of Infineon Technologies, said that IGBT technology, a representative of silicon-based power semiconductors, has encountered some difficulties in further improving performance. Switching loss and conduction saturation voltage drop reduction mutually restrict each other. The space for reducing losses and improving efficiency is getting smaller and smaller, so the industry begins to hope that SiC can become a disruptive technology.

But this view is not very comprehensive. Taking Infineon silicon-based IGBT as an example, he said that with the advancement of packaging technology, the performance and power density of IGBT devices are getting higher and higher. At the same time, products developed for different applications can undergo some special optimization processing to improve the performance of silicon devices in the system, thereby improving system performance and cost performance. Therefore, the development process of third-generation semiconductors must be accompanied by silicon devices. "In addition to technological development, there are also considerations of large-scale commercialization value factors for different applications. It is unrealistic to expect that third-generation semiconductor devices can quickly replace silicon devices in all application scenarios."

Ajay Hari, director of AC-DC applications at ON Semiconductor, said:

Ajay Hari, director of AC-DC applications at ON Semiconductor, believes that in the long run, SiC will defeat IGBT. Of course, in some price-sensitive applications, IGBT will be given priority. In the next 3-5 years, as SiC becomes more competitive, it will seize areas previously occupied by IGBTs. “Using voltage as a reference, when the voltage is 650 V, SiC outperforms GaN and SJ MOSFETs. However, compared to SiC and SJ MOSFETs, GaN is a higher frequency material, so GaN is more It is suitable for consumer and IoT applications, such as USB PD (power supply) and games. The 650 V SJ FET will be classified into lower-profit applications; the 100V and below GaN and silicon field effect transistors will be long-term coexistence in medium-voltage applications,” he said.

Senior manager of the Semiconductor Technology Management Department/Technology Planning Department of Toshiba Electronic Components (Shanghai) Co., Ltd. said:

Compared with silicon (Si), silicon carbide (SiC) is a semiconductor material with greater dielectric breakdown strength, faster saturated electron drift, and higher thermal conductivity. SiC devices can provide high withstand voltage, high-speed switching and low on-resistance when used in semiconductor devices. Huang Wenyuan, senior manager of the Semiconductor Technology Management Department/Technology Planning Department of Toshiba Electronic Components (Shanghai) Co., Ltd., believes that SiC is regarded as a new generation material for power devices, which will help reduce energy consumption and reduce the size of the system.

However, the upstream and downstream suppliers and device manufacturers of the silicon carbide industry still need to be improved, and this process will last for a long time. During this period, Si and SiC devices will complement each other and coexist. Some products that have higher requirements for switching frequency, withstand voltage, and power loss and have relatively loose costs will give priority to SiC devices, while other products will continue to use Si devices. .

Alex Zahabizadeh, product marketing engineer at Texas Instruments (TI) Automotive Gallium Nitride High Voltage Power Division, said that "complementary symbiosis" is a good word to describe the future competitive characteristics of power semiconductor devices, which can be found on the primary side (transformer or High-voltage to low-voltage DC/DC converters using gallium nitride (GaN) on the input side of the transformer) and IGBTs on the secondary side (output side of the transformer or transformer). "The advantages of GaN can be maximized in designs that require higher efficiency and smaller size. As electric vehicles advance, we see GaN as an ideal solution for on-board chargers and DC/DC converters."

Electric power technology calibration

"In the field of 600V-1700V voltage applications, SiC MOSFET has greater performance advantages compared with Si MOSFET and IGBT. As semiconductor companies continue to build new SiC manufacturing lines, the price of SiC power devices will continue to decline, but Si technology It will also become more mature, and there will be a price difference between SiC devices and Si devices for a long time. Of course, the high market demand for SiC MOSFETs will prompt users to accept this price difference." Cissoid Chief Technology Officer Pierre Delatte said that through system-level performance and cost benefits to justify the transition to SiC devices. "The reduction in conduction and switching losses and excellent thermal performance will promote SiC technology to gradually replace Si technology. SiC will play a role in applications where battery efficiency and weight/volume are critical."

Power technology calibration Image source: TI

Pierre Delatte, CTO of Cissoid

The current cost of SiC substrate wafers is 4 to 5 times that of Si substrate wafers of the same size. It is expected that in the next 3 to 5 years, the price of SiC substrate wafers will gradually drop to about 2 times that of Si. In this process, tight production capacity and supply of SiC devices may be inevitable in the short term. According to analysts at "International Electronic Business News", whether it is SiC or GaN, although they have superior performance in many application scenarios, they still face some constraints on the path to large-scale commercialization.

Bottlenecks restricting the commercial use of third-generation semiconductors

As silicon-based devices approach the critical point of cost-effectiveness, mainstream power semiconductor device manufacturers are exploring third-generation semiconductor materials. There is also a voice in the market saying that third-generation semiconductors will completely replace silicon devices, but this will not happen in the short term.

Power device manufacturer Infineon has been working on SiC for the past thirty years: in 1992, it began to develop SiC power devices; in 1998, it established a 2-inch production line; in 2001, it launched its first SiC product; in 2006, it released MPS technology diodes; in 2013, it took the lead in adopting fifth-generation thin wafer technology; from 2014 to 2017, it successively released SiC JFET, fifth-generation 1200V diodes, 6-inch technology and SiC trench gate MOSFET.

From the development history of Infineon SiC devices, we can see the development history and trends of SiC technology. Chen Ziying said: "We are well aware of the reliability issues of planar gates. Before the development of trench gates is completed, SiC JFET is a transitional product to help customers quickly enter the SiC application field. From the perspective of technology development trends, SiC MOSFETs are better than IGBTs. There is a more urgent need to move to trench gates, focusing more on reliability issues in addition to power density considerations.”

Cheng Wentao, Director of Application Marketing, Greater China, Power and Sensing Systems Division, Infineon Technologies

"In the third decade of the 21st century, the third-generation semiconductor industry pattern has undergone tremendous changes - the SiC industry is accelerating vertical integration, and the GaN industry has formed a coexistence of IDMs, design companies and wafer foundries. model." Cheng Wentao, Greater China Application Marketing Director of Infineon Technologies Power and Sensing Systems Division, said, "Of course, the industry development time of the third generation semiconductor is relatively short, and there is still a long way to go in terms of standardization and maturity. There is still a lot of research and validation work to be done, especially in terms of quality and long-term reliability.”

In order not to miss every possibility of technology implementation, powerful companies often take the path of keeping pace with multiple technologies. Companies such as Infineon, ON Semiconductor, and Toshiba have three main power technologies: Si, GaN, and SiC. They can be completely customer-oriented. For such companies, balancing investment in different power devices at different stages is a very important task.

Zhong Xiaolong, senior director of the Greater China Automotive Electronics Division of Infineon Technologies and head of the Power and New Energy Systems Business Unit, said that in addition to IGBT products that are well-known in the new energy vehicle market, Infineon is also in the field of third-generation power semiconductors. With scientific layout and active expansion of product lines, customers can choose the most suitable devices according to their needs and build their own systems.

Cheng Wentao added that as the industry pursues higher energy efficiency, energy conservation and emission reduction, if it is to continue to develop at the current speed, wide bandgap materials such as SiC and GaN are the most promising innovative technologies to succeed silicon devices. In recent years, Infineon has increased investment in the research and development and production of wide bandgap technology, and it is expected that more new wide bandgap products will be launched at an accelerated pace in the next few years.

Jon Harper, Director of Application Engineering, ON Semiconductor Power Solutions Division

On August 25 this year, ON Semiconductor announced that it would acquire SiC manufacturer GT Advanced Technologies (GTAT) for US$415 million in cash. Jon Harper, director of application engineering at ON Semiconductor’s Power Solutions Department, said the deal is to support customer demand for SiC devices. It is expected that by 2028, electric vehicle sales will account for 50% of automobile sales. SiC is one of the very important materials for electric vehicles. In order to ensure that there is enough SiC production capacity in the market, ON Semiconductor will accelerate the development of SiC products. He also added that SiC and GaN are complementary technologies and ON Semiconductor is optimistic about them. SiC is suitable for high current applications of 650 V, 900 V and 1200 V, and GaN is suitable for high switching frequency applications below 650 V.

Toshiba's SiC power devices are mainly used in train inverters, and the devices are expected to be used in photovoltaic power generation systems and power management systems in the future. However, the lifespan and market growth of SiC devices have been hindered by product reliability issues. Huang Wenyuan explained, "When current flows through the PN diode between the source and drain of the power MOSFET, it will amplify its crystal defects, increase the on-resistance, and reduce the reliability of the device. To this end, Toshiba has developed a new The device structure is a Schottky barrier diode (SBD) embedded MOSFET. By placing an SBD in parallel with the PN diode in the MOSFET to prevent the PN junction diode from operating and ensuring a lower on-state voltage, the conduction can be suppressed. Changes in resistance."

GaN power devices are candidate devices for achieving system efficiency and miniaturization. They are mainly used in fast chargers for smartphones and computers, and are expected to be used in power supplies for industrial equipment and servers in the future. GaN transistors used for power conversion can be divided into two types: cascode and p-GaN gate. The latter uses a p-GaN gate to keep the GaN HEMT in a normally off state. Toshiba's new GaN cascode device has a higher threshold voltage than p-GaN gate normally-off HEMT devices, is less susceptible to noise, and does not require a specific driver IC.

Alex’s point of view focuses on the commercial bottlenecks of GaN. The bottlenecks that restrict the large-scale commercialization of GaN include design experience, development and learning time, and changing market demands. "Many engineers have only heard of GaN in news reports or new product promotions, but lack experience in designing with it. TI provides many evaluation kits to test the performance of GaN to help customers start designing products using GaN for the first time."

Pierre believes that production capacity is the bottleneck limiting the commercial use of SiC. Today, the delivery time of SiC devices generally exceeds 6 months. Although the tight supply situation will improve with the addition of new factories. But in the meantime, demand will boom, especially from the electric vehicle industry. You can still expect several years of market turmoil before prices and demand achieve a balanced match.

Another obstacle to SiC and GaN commercialization is the “learning curve of designing new power converters.” These new fast switching transistors bring new challenges to the design and key components of power modules. Cissoid has launched a three-phase SiC intelligent power module (IPM) platform that relies on the co-design of power modules and gate drivers to adjust dV/dt and control the voltage overshoot inherent in fast switching, optimizing for the lowest switching energy.

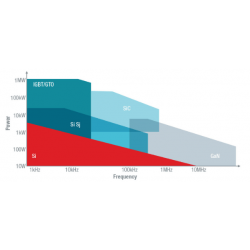

Is SiC technology ahead of GaN?

Taking the Chinese market as an example, China has achieved mass production of 4-inch SiC substrates and completed the research and development of 6-inch SiC substrates. However, the preparation technology of GaN needs to be improved. Currently, it can only produce 2-inch GaN substrates in small batches and has the production capacity of 4-inch GaN substrates. In the view of some interviewees, since the two are suitable for different application scenarios, they cannot be viewed in a competitive relationship, but other interviewees agree that SiC’s commercial use has exceeded GaN.

Huang Wenyuan said that although SiC and GaN both have the advantages of high withstand voltage, small on-resistance, and small parasitic parameters, they also have different characteristics. For example, GaN has extremely small parasitic parameters and extremely high switching speed, making it suitable for high-frequency applications. The easy-to-drive characteristics of SiC MOSFET make it suitable for high-performance switching power supplies and can improve the efficiency and power density of switching power supplies. Judging from the market application status, both GaN and SiC have specific applications in progress, and SiC technology seems to be slightly ahead. It is certain that both GaN and SiC are indispensable and good technologies, but there may be slight differences in application fields. Where the application system requires higher frequency, GaN may be better, and where the operating environment temperature is higher, SiC may be more suitable.

“Both GaN and SiC are gradually developing towards 6-inch and 8-inch wafers to help reduce costs and increase production capacity. It is difficult to judge which of the two technologies is more advanced.” Alex added: “We can provide both Gate drivers designed with SiC field effect are also continuing to promote the design of silicon-based GaN and bring competitive products to the market." It is understood that TI produces GaN devices on silicon-based GaN substrates through its own factories. Helping the company reuse existing silicon tools and gain supply chain advantages.

Last October, TI launched its next-generation 650V and 600V GaN FETs for automotive and industrial applications. For automotive-grade third-generation semiconductor devices, other manufacturers are choosing to use SiC more, while TI is launching GaN devices for cars. The LMG3522R030-Q1 launched by TI is the first automotive-grade GaN device with integrated driver. Compared with existing Si and SiC solutions, the GaN device design provides better switching performance indicators, is more efficient and is smaller. Small. Alex believes that future electric vehicles will utilize both GaN and SiC technologies - GaN is mainly used in AC/DC on-board chargers and high-voltage DC/DC converters, while SiC is mainly used in automotive traction inverters and compressors.

Especially in terms of 600V-1700V application voltage and high current, SiC technology is more mature than GaN. Pierre said: "The SiC gate drivers and SiC smart power modules provided by Cissoid are mainly used for voltages in the range of 600V-1700V and currents up to 600A. In 2013, Cissoid also launched a SiC power MOSFET package, which can Operating at 225°C. However, GaN technology is not yet mature in this regard because GaN transistors switch extremely fast, which makes the design of large power modules and their gate drivers more complex and currently cannot be applied to this power range. Device mass production products. We are using the experience gained from SiC to prepare new solutions for advanced GaN power modules and gate drivers."

If we only look at the commercial production of market segments, we can see that GaN has already begun to be used in the consumer fast charging market. Referring to market analysis data from CITIC Securities, the GaN fast charging market will rise to 63.8 billion yuan in 2025, with a CAGR of 94% from 2021 to 2025. In addition, after the outbreak of the new crown epidemic, the demand for global 5G base station construction has accelerated, stimulating the popularization of radio frequency GaN and power GaN applications. Driven by consumer electronics and 5G infrastructure, the cost of GaN products has dropped, and application scenarios will be further expanded to new energy vehicles, lidar, data centers and other fields.

In addition, SiC has also been well applied in the field of automotive electronics. According to forecasts from HIS Markit, the market size of SiC power devices is expected to exceed US$10 billion by 2027, with a compound annual growth rate of nearly 40% from 2018 to 2027. Among them, the new energy vehicle market is the most important driving force.

Trends of power semiconductors in the next five years

According to reports from the channel chain, since power semiconductors mainly rely on 8-inch wafer manufacturing capacity, coupled with the continued growth of electric vehicle shipments, the demand for power semiconductor devices has surged, resulting in obvious shortages and price increases.

Infineon interviewees stated that current demand continues to remain at extremely high levels and greatly exceeds supply, and shortages are expected to continue into 2022. As structural drivers, the energy transition and digitalization are continuing to generate consistently strong demand. As before, global supply chains remain strained. At the same time, semiconductor inventories are at historically low levels and many applications and most end markets are experiencing delivery bottlenecks. The global COVID-19 pandemic has not yet been overcome and will continue to be a source of uncertainty.

Cheng Wentao said that from the perspective of power device demand, areas with strong growth in the future include: new energy vehicles and their supporting industries, big data (data centers), communication infrastructure, photovoltaic power generation, smart grids, industrial equipment, smart homes, etc. Infineon will continue to lead the technological development direction of power semiconductors by virtue of its scale effect, coupled with years of technology accumulation and continuous investment.

In early August this year, ON Semiconductor announced a high-profile name change. Ajay said: “We have identified growth areas in ‘smart power’ and ‘smart sensing’. ‘Power’ and ‘sense’ are a winning combination and together they are driving massive disruption in the industrial and automotive markets. Climate and sustainability Sustainability is a key demand driver for electrification and power efficiency, and energy-efficient electricity production, distribution and consumption will be key to the future."

Citing forecasts from the International Energy Agency (IEA), Jon said that the strong growth of electric vehicles is a factor driving the semiconductor market, and solar inverters and energy storage are also continuing to grow, which is in connected equipment, data centers, industrial automation and beyond the needs of self-driving cars. During this period of strong growth, it is important to consider the semiconductor market, and even the electronic components market as a whole, as shortages in one area will reduce demand in other areas. The SiC and GaN markets are expected to see strong but highly volatile growth.

ON Semiconductor's interviewees also predicted future trends in power semiconductor devices. “Electric vehicles, along with their on-board chargers and other on-board power systems, will become widespread users of power semiconductors; EV charging infrastructure supported by solar and wind energy stored in energy storage systems will be driven by strong growth in EVs; machines The growth of data centers driven by demand for learning, cloud computing and online services will drive the use of more reliable uninterruptible power supplies (UPS) and GaN-based power strips for power distribution in these data centers."

Cissoid's Pierre said that today's lead times for power electronic components typically exceed six months, and for some components can even be closer to a year. With the transition from fuel vehicles to electric vehicles, according to statistics from Strategy Analytics, the power device content in pure electric vehicles has reached 55% as early as 2019. Of course, the transition to SiC and GaN technologies will also continue, and even accelerate. The demand for higher power density devices will push power devices to withstand higher junction temperatures and packaging technology to be more reliable at high temperatures. This also affects all components used in the power converter, including gate drivers, DC bus capacitors, sensors, etc.

TI believes that GaN will be more widely used in the next 10 to 20 years. Alex said: "Today, servers, computers and industrial power supplies using GaN are already in use, and in five years it will achieve wider commercial applications. GaN will also be more widely used in other industrial markets such as robots and motor drives during the same period. into the commercial market, such as in vehicle chargers and high-voltage DC converters.